How much down payment is best for my purchase?

This is the most common question that we get from United States Veterans, active-duty service members, reservists, and their spouses that are eligible for VA home loans.

This blog article explores this topic from multiple angles (financial and non-financial) and will provide some guidance on the best overall strategy.

Should I put 0% down?

VA home loans are common in certain areas of the US, especially near large military bases. In these areas, local realtors are accustomed to receiving offers that fully leverage the 0% down payment privilege offered by VA mortgages. As a NJ Mortgage Broker, we have the exact opposite experience. There are only a few military bases in New Jersey, none of which are active duty military bases, so realtors receive VA offers much less frequently.

In areas in New Jersey like Bergen County, the real estate market competition is especially fierce, with 5 – 50 offers on every single home listed on the NJMLS. In northern New Jersey, 0% down payment loans of any type (VA, USDA, FHA, or non-traditional loans) are rarely preferred by sellers and their realtors. The reason is that many sellers and realtors believe that anyone who chooses a mortgage loan with no down payment is less creditworthy than other buyers with large down payments. Although this may not actually be the truth, it is a perception that influences behavior, making it especially difficult to get your offer accepted in these areas with a 0% down payment loan.

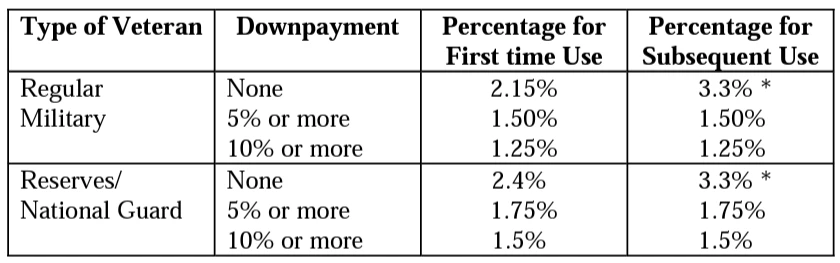

The other disadvantage of 0% down payment is a higher funding fee for non-exempt (non-disabled) veterans. On February 14, 2023 the Veterans Benefit Administration and Department of Veterans Affairs issued Circular 26-23-06, which updated the funding feeing fees for VA loans closed on or after April 7, 2023. The portion of the table specific to VA purchases is snipped below:

(Source: VA Pamphlet 26-7, Revised)

As you can see in the table above, the VA funding fee is larger for a 0% down payment (downpayment is “None” in the table) than if you are able to allocate 5% or 10% towards a down payment.

Should I put 5% or 10% down for a VA home loan?

The remainder of this article is a mathematical comparison of each option (0%, 5%, and 10% down payment), and which is the best option if you are pursuing a VA home loan.

Let’s start with the most common scenario:

Example of a VA Home Loan Profile

· First Time Home Buyer (first use of VA benefit)

· Regular Military

· Not Exempt from Funding Fee (non-disabled)

· $400K purchase price

· Same interest rate regardless of down payment percentage (this is common for VA loans)

Option 1: 0% Down

Down Payment = $0

Funding Fee = $400,000 x 2.15% = $8,600

Option 2: 5% Down

Down Payment = $400,000 x 5% = $20,000

Funding Fee = $380,000 x 1.5% = $5,700

Option 3: 10% Down

Down Payment = $400,000 x 10% = $40,000

Funding Fee = $360,000 x 1.25% = $4,500

Assuming that you have enough funds (at least $40,000) for any of these options, which one should you choose?

The answer is that it depends on the interest rate on your mortgage, as well as what you would do with the money if you did not use it for down payment. How would you have otherwise invested it if you hadn’t used it for your down payment?

Let’s assume that you are a conservative investor, and you would put your funds into a 2-year CD if you didn’t use them for down payment (this way, your funds are GUARANTEED to increase and there is no risk, as the CD is insured by FDIC). A quick Google search indicates that you could earn 4.85% APY as of 6/13/23.

Our next assumption is that you will own your property for at least 2 years before you sell it (this is a safe assumption for most homeowners).

Our last assumption is that your interest rate on your VA home loan is 6.125%, and that you don’t make any extra payments in your first 2 years (6.323% APR as of 6/13/23).

In this case, if you choose 0% down payment, you could put all $40,000 of your savings into the CD, and in two years you would earn:

[ ($40,000 x 1.0485 x 1 year) x (1.0485 x 1 year) ] - $40,000 = $3,974.09.

Here is the math for 5% down payment:

5% Down:

[ ($20,000 x 1.0485 x 1 year) x (1.0485 x 1 year) ] - $20,000 = $1,987.05.

So which option is best, assuming you sell your home after 2 years of ownership?

|

|

Option 1: 0% Down |

Option 2: 5% Down |

Option 3: 10% Down |

|

Funding Fee |

$8,600 |

$5,700 |

$4,500 |

|

Total Interest for First 2 years of Mortgage |

$49,472 |

$46,700 |

$44,133 |

|

Interest Earned on 2 YR CD at 4.85% |

-$3,974 |

-$1,987 |

$0 |

|

Net Amount Spent on Interest and Fees |

$54,098 |

$50,413 |

$48,633 |

What about after 4 years of ownership?

|

|

Option 1: 0% Down |

Option 2: 5% Down |

Option 3: 10% Down |

|

Funding Fee |

$8,600 |

$5,700 |

$4,500 |

|

Total Interest for First 4 years of Mortgage |

$97,631 |

$92,159 |

$87,094 |

|

Interest Earned on |

-$7,246 |

-$3,623 |

$0 |

|

Net Amount Spent on Interest and Fees |

$98,985 |

$94,236 |

$91,594 |

Summary:

Option 3 (10% down payment) will always be the lowest cost option in our example.

There are a few reasons why 10% down payment is the best option for VA Home Loans:

1. The interest rate for our investments of the down payment (4.25% - 4.85%) is lower than the interest rate on the mortgage (6.125)%.

2. Veterans pay interest on the funding fee amount (the fee is added to the loan balance and financed over 30 years).

3. The amount of the funding fee (as a percentage of the loan) is larger with 0% down payment than it is at 5% or 10% down payment due to circular 26-23-06.

Do you need help calculating the right down payment percentage for your VA Home Loan? If you are buying a home in New Jersey, we would love to be your NJ Mortgage Broker.

Recent Articles

-

Mortgage Pre-Approval in New Jersey: Your Complete Guide

7/14/2026 12:00:00 AM

7/14/2026 12:00:00 AM

-

How to Buy a Home in New Jersey

6/17/2026 12:00:00 AM

-

Top 5 Reasons Pre-Approved Mortgages Get Denied

9/12/2023 8:57:26 AM